Developing a Financial Economics Course

By Emiliano A. Carlevaro

Between 2024 and 2025, I redeveloped the Financial Economics course at the University of Adelaide. The course is nominally a second-year course, but it has very few prerequisites: students are only required to have completed a basic mathematics course, with no requirement to have taken calculus or even Principles of Economics. In practice, most students have some introductory economics background, but the cohort still includes students with very different levels of preparation.

Landing page. Main page of the course in Canvas LMS.

Alas one of the main challenges was student heterogeneity. For Bachelor of Economics students, the course is usually taken in the first semester of their second year. For Bachelor of Commerce students, it can be a first-year course, often taken concurrently with Principles of Economics. For students in Finance degrees, it is usually a third-year course. For students doing a double degree in Engineering and Finance, it can be a fifth-year course.

As a result, the classroom includes students ranging from recent school-leavers to students with work experience, and from students with no calculus background to students with advanced quantitative training.

The course typically enrolls around 100–125 students. It runs over 12 weeks, with two face-to-face sessions per week: a 90-minute lecture and a 50-minute practical tutorial.

Course content for everybody

Since calculus could not be assumed, I followed the general approach of Hal Varian’s Intermediate Microeconomics textbook1, which develops many key ideas without relying heavily on calculus. However, to keep more quantitatively prepared students engaged, I also included optional appendices with calculus-based proofs and solutions, such as Lagrangian solutions to utility-maximisation problems.

These appendices proved useful for Finance and Engineering students, who often found it easier to rely on familiar calculus-based arguments than on discrete, step-by-step reasoning.

The course is divided into three main parts:the demand for safe assets, the demand for risky assets, financial crises.

The demand for safe assets

The first part covers the core microeconomic tools needed to study financial decisions: the consumer choice problem under certainty, budget constraints, preferences, utility and choice. It concludes with Intertemporal choice, which brings these concepts together in a setting directly related to saving and asset demand.

The structure broadly follows Varian’s textbook, but with a stricter focus on the concepts and examples most relevant for financial decision-making.

The demand for risky assets

The second part introduces decisions under uncertainty. It begins with basic concepts such as dominated strategies and decision rules, before moving to the expected utility framework.

Following Kolmar’s textbook2, I also discuss the historical development of the theories. This historical perspective helps students understand why different frameworks emerged and why expected utility became so central.

The course then introduces asset pricing using the consumption-based asset pricing model, drawing on John Cochrane’s magnum opus Asset Pricing textbook3. This connects the consumption decisions studied at the beginning of the course with asset prices.

Asset-pricing models are presented in two ways: first as the result of optimal demand for risky assets, and later through the stochastic discount factor. This helps connect the language of finance with the economic theory students have developed throughout the course.

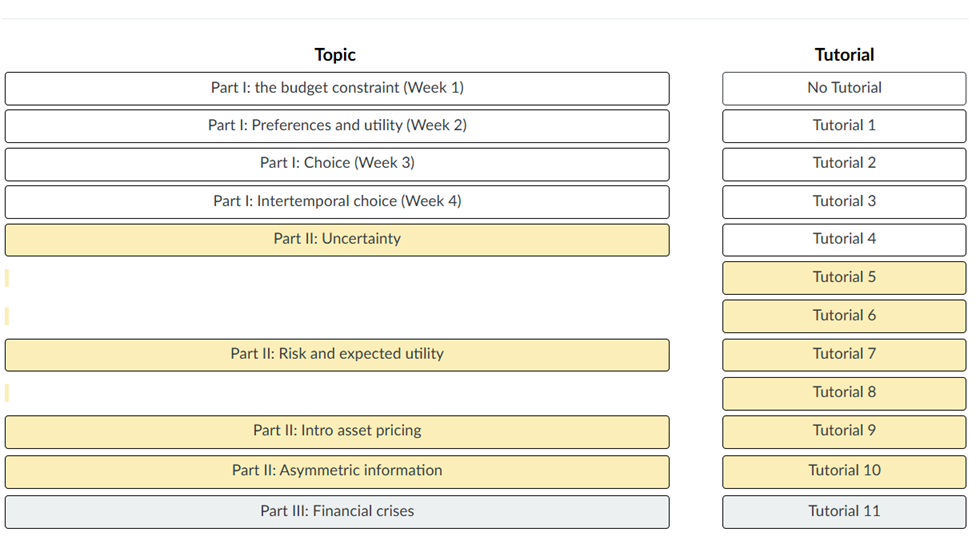

SIMPLE MAIN MENU. The 3 parts of the course are colour-coded, with most course content accessible in fewer than 3 clicks.

Financial crises

The final part applies the concepts developed throughout the course to financial crises around the world and in Australia. Students use ideas from asymmetric information, risk, asset pricing and intertemporal choice to understand the mechanisms behind financial instability.

Assessment for everybody

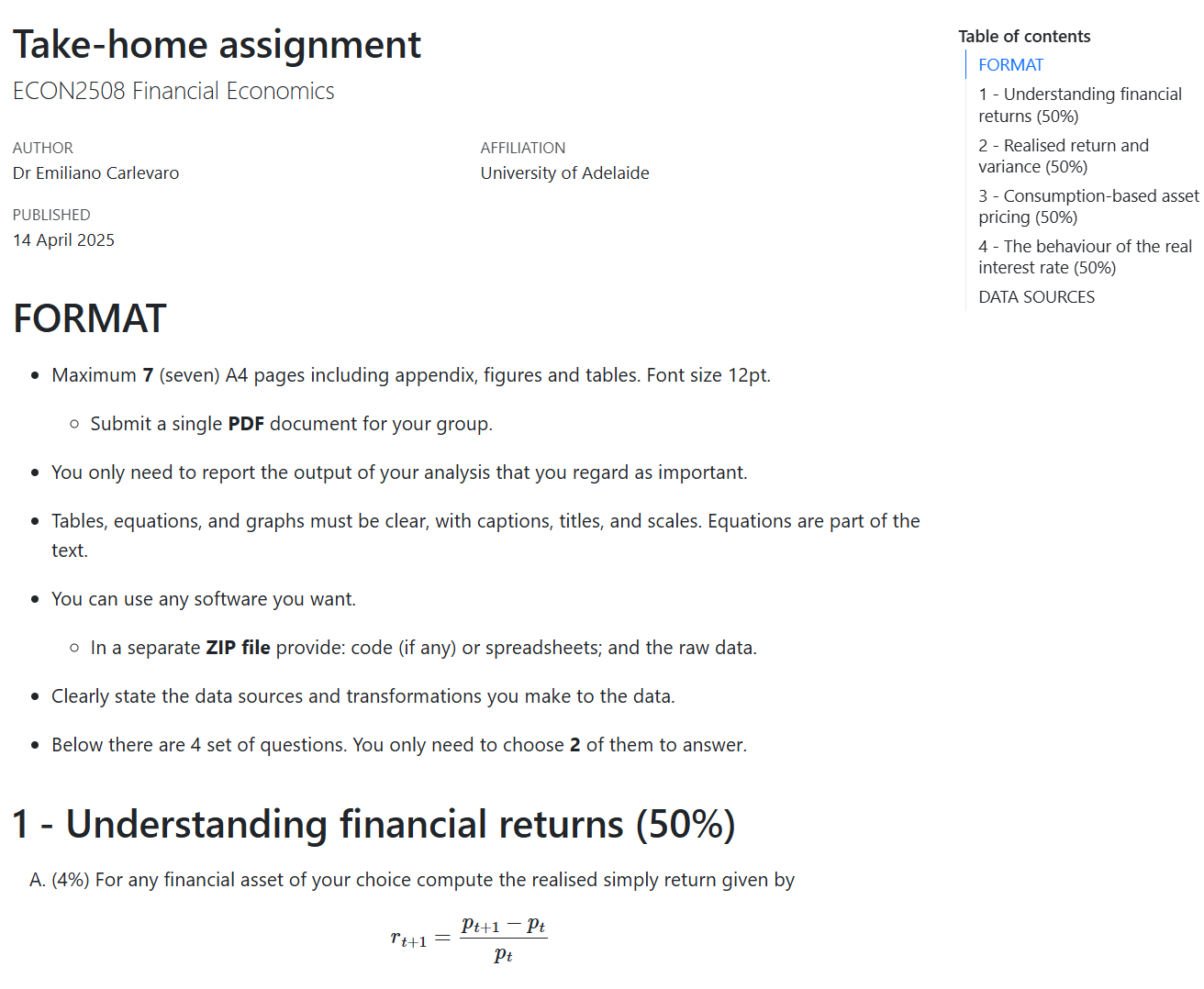

After redesigning the content, the next challenge was assessment. I designed the major assignment so that students could self-select into problems that matched their interests and level of preparation.

For example, the Group Assignment includes four different problems requiring different skills. Some problems require statistical knowledge, while others rely more on introductory macroeconomics or conceptual reasoning. This structure allows students to engage with financial economics from different entry points.

The assignment is also deliberately empirical, which helps offset the rather substantial theoretical nature of the course core content.

ASSIGNMENT FOR HETEROGENEOUS STUDENTS. Students choose a problem suited to their background and interests. Some problems require statistical skills, while others rely on introductory macroeconomics.

References to popular culture

During the course, I use examples from popular films and TV series to motivate key ideas. For example, to introduce the empirical component of the assignment, I refer to the line “Theory will only take you so far” from Oppenheimer (2023).

When discussing probabilities in the expected utility framework, I use a scene from Friends in which Ross reacts to the claim that condoms work 97% of the time: Ross Yells at a Condom Company | Friends.

These references help make abstract concepts more memorable and create a more accessible entry point for students.

Markdown throughout

All course material is written in Markdown. This has three main advantages:

- other teachers can easily edit the material;

- a single source file can be rendered to PDF, HTML or PowerPoint;

- text can be kept separate from supporting resources such as images and videos.